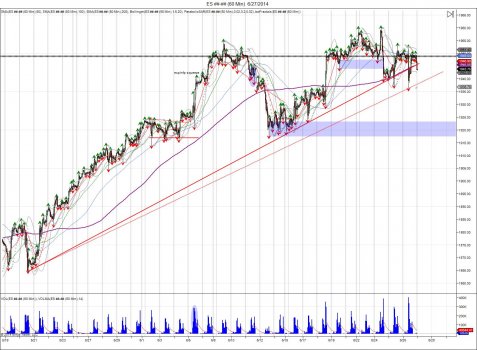

SP500 futures have been in limbo after completing the 1955 target based off the January-February range expansion (1844-1732 = 112, 1844+112=1956). This level has also coinciding with a major fib extension at 76.4% based off the May 2013 low (1553) to the December 2013 high (1846) and the February 2014 low (1732).

We know this year started off sideways from last years close, which was followed by a massive liquidation from 1844 down to 1732. This selloff was reversed, with the market recovering above 1844 to squeeze out shorts. The reversal above 1844 created the plateau to allow new buyers to come in and support prices to attempt and expand the 112 point move down up into 1956. After 3 months of sideways consolidation and bear traps, the market printed new highs in May at 189850 followed by a low of 1859 that barely held its May low of 185450. By holding this low, the market managed to reverse and squeeze through 1898, giving way to breaking outside of the 3 month range and expanding up to complete the target as shorts once again were squeezed. The ECB came out on the 5th of June to cut rates to negative, giving the boost in the SP to hit 1940. The following day was the Jobs report on the 6th of June which continued the move into highs of 184975. Spilling over into Monday, highs of 195475 were made completing the range expansion and meeting the 76.4% fib, give or take a point. The futures rollover from June into September saw prices rollover with, falling down into 1917 to test the June lows and hold, before reversing back up as the September contract became the front month and went toward to meet with its 76.4% fib as well.

Highs of 195975 were made during last Sunday's Globex session that further squeezed shorts after September took out the continuous highs. Since this Globex high, the cash market opened lower only to rally back and retest this high, making a new one by a tick at 1960 before going offered down to 1936. Over the past 2 trading days the SP has fought to hold above 1940 as it attempts to defend the reversal off the 1917 lows and develop a base to squeeze shorts through 1960. Buyers at the 1940 level need a move through 1960 to be rewarded based on their risk of defending the 1917 low. Doing so, gives way to the next major fib level of 100% at 2025. Failure to hold 1940, gives way down to target the 1917 low made last week. Failure to hold 1917 confirms the new highs as a failed breakout with buyers that will be forced to liquidate which gives way down to retracing into the May breakout at 1890 to allow buyers to defend. This would be alot healthier to the market as it would allow buyers a opportunity to buy a dip and use a break of the May lows as their exit, as opposed to forcing buyers to chase above 1960 in which will continue the capitulation of shorts and parabolic squeeze. It is the struggle to accept 1950.

It is important to pay attention to VIX futures here. After taking out multi year lows and falling below its trend line from the 2013 lows, VIX fell into 1073 early June, before bouncing up to 1289 in an attempt to come back. This early attempt was rejected and VIX was sold down to make new lows (as the SP made new highs), falling down to 1034 before seeing a push back to highs of 1233 on the 25th of June. It is interesting to note the take of the Volatility Sonar report from Optionmonster TV that highlights July call sellers in the VIX futures and an absent of what they call the "call stupid buyer" that has been buying premium in VIX not show up on that particular weakness from the 25th. Jamie Tyrell explains how VIX can turn higher toward the end of the video. Thursday saw VIX press against highs of 1251, nearing that 1289 June high, before backing away. Shorts in Vol should be concerned as a squeeze through the June highs forces shorts to cover as the June lows setup a failed breakdown, giving way for a move to retest the April range of 16-18.

This was our projection of VIX just a little over a month ago: http://stks.co/p0M9e

Optionmonster TV $VIX Sonar Report:

Hourly SP500: